The expanding request inside the worldwide market for cloud access security dealers has been ascending because of the developing requirement for network protection across numerous industries. The vendors existing in the worldwide market for cloud access security intermediaries have put forth fervent attempts to persuade the customers of the validity of their administrations. Cloud-based administrations have acquired prevalence across the globe, and the vendors have shown crabbiness in utilizing this pattern for their potential benefit. Various new vendors have recently gone into the worldwide market for cloud access security agents market, and every one of them is on a journey to amplify their incomes.

The worldwide market for cloud access security is relied upon to observe an exceptional degree of rivalry among the market players throughout the next few years. This projection can be clarified as far as the voluminous interest for cloud administrations across different industries. The market vendors are zeroing in on procuring key compensations by catching the markets of enormous industries and areas. Moreover, the medium-sized vendors existing in the worldwide market for cloud access security dealers are additionally expected to fall back on consolidations and acquisitions. Cloud figuring innovation is acquiring a foothold inferable from its capacity to examine, screen, and store information continuously. In this way, the ascent in the reception of cloud processing innovation is making beneficial business roads in the worldwide cloud access security dealers market.

The flood in mindfulness with respect to various innovations that can help associations in putting away colossal measures of information in one area is assessed to set out worthwhile open doors in the worldwide cloud access security intermediaries market in the years ahead. Besides, the development and reception of mechanical progressions, for example, AI and IoT are probably going to assume a critical part in the extension of the cloud access security representatives market in the gauge time frame.

The sending of cloud access security representatives is in effect progressively done across SaaS stages because of the flood in the patterns in SaaS-conveyed benefits along with their expense productive nature. The ascent in the requirement for the capacity of significant data and information connected with states, organizations, and associations has brought about an increment in the utilization of a strong net of security. This component is energizing the development of the worldwide cloud access security specialists market.

The global cloud access security brokers market is classified on the basis of cloud deployment type, components, and regions. Based on cloud deployment type, the market is grouped into infrastructure as a service (IaaS), platform as a service (PaaS), and software as a service (SaaS). The components segment is trifurcated into cloud-based software, on-premise software, and services software. The cloud-based and on-premise segments are each grouped into tokenization, data leakage prevention cloud data encryption, risk & compliance management, and control & monitoring. The services segment is categorized into operation and maintenance, system integration, and consulting.

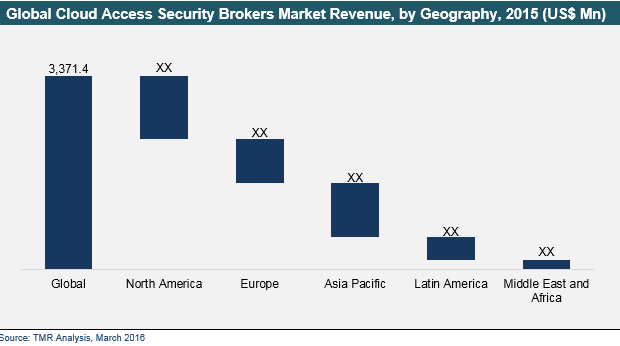

Some of key locales of the worldwide cloud access security merchants market incorporate North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. Of them, North America is overwhelming market area, which is projected to grow at a CAGR of 18.4% during the gauge time frame. This development can be credited to many variables remembering the ascent for utilization of cloud-empowered administrations in the U.S. Also, flood in mindfulness in regards to cloud security is setting out promising open doors for the provincial market development.

The presence of a few central participants makes the opposition levels in the cloud access security agents market profoundly serious. In this manner to support in the high contest, organizations are using various procedures including consolidations, acquisitions, associations, and joint efforts. Also, organizations are centered around the extension of their organizations in more current areas.

Players in the cloud access security specialists market are expanding endeavors to work on the nature of administrations they offer. Consequently, they are seen expanding cash in-stream toward R&D projects. Such drives are probably going to fuel market development in the impending years. A portion of the vital participants working in the worldwide cloud access security dealers market are Adallom, Inc., Zscaler, Inc., Skyhigh Networks, Bitglass, Inc., NetSkope Inc., CipherCloud Inc., CloudLock Inc., and Protegrity USA, Inc.

1. Preface

1.1. Report Description

1.2. Research Scope

1.3. Market Segmentation

1.4. Research Methodology

2. Executive Summary

2.1. Global Cloud Access Security Brokers Market Snapshot

2.2. Global Cloud Access Security Brokers Market Revenue, 2014 – 2024 (US$ Bn) and Year-on-Year Growth (%)

3. Global Cloud Access Security Brokers Market Analysis, 2014 – 2024 (US$ Bn)

3.1. Overview

3.2. Market Dynamics

3.2.1. Drivers

3.2.2. Restraints

3.2.3. Opportunities

3.3. Key Trends Analysis

3.4. Global Cloud Access Security Brokers Market Analysis, By Components, 2014 – 2024 (US$ Bn)

3.4.1. Overview

3.4.2. Software

3.4.2.1. On-premise

3.4.2.1.1. Control and Monitoring

3.4.2.1.2. Risk and Compliance Management

3.4.2.1.3. Cloud Data Encryption

3.4.2.1.4. Data Leakage Prevention

3.4.2.1.5. Tokenization

3.4.2.2. Cloud

3.4.2.2.1. Control and Monitoring

3.4.2.2.2. Risk and Compliance Management

3.4.2.2.3. Cloud Data Encryption

3.4.2.2.4. Data Leakage Prevention

3.4.2.2.5. Tokenization

3.4.3. Services

3.4.3.1. Consulting

3.4.3.2. System Integration

3.4.3.3. Operation and Management

3.5. Global Cloud Access Security Brokers Market Analysis, Cloud Deployment Type, 2014 – 2024 (US$ Bn)

3.5.1. Overview

3.5.2. Software as a Service (SaaS)

3.5.3. Platform as a Service (PaaS)

3.5.4. Infrastructure as a Service (IaaS)

3.6. Competitive Landscape

3.6.1. Market Positioning of Key Players, 2015

3.6.2. Competitive Strategies Adopted by Leading Players

4. North America Cloud Access Security Brokers Market Analysis, 2014 – 2024 (US$ Bn)

4.1. Overview

4.2. North America Cloud Access Security Brokers Market Analysis, By Components, 2014 – 2024 (US$ Bn)

4.2.1. Overview

4.2.2. Software

4.2.2.1. On-premise

4.2.2.1.1. Control and Monitoring

4.2.2.1.2. Risk and Compliance Management

4.2.2.1.3. Cloud Data Encryption

4.2.2.1.4. Data Leakage Prevention

4.2.2.1.5. Tokenization

4.2.2.2. Cloud

4.2.2.2.1. Control and Monitoring

4.2.2.2.2. Risk and Compliance Management

4.2.2.2.3. Cloud Data Encryption

4.2.2.2.4. Data Leakage Prevention

4.2.2.2.5. Tokenization

4.2.3. Services

4.2.3.1. Consulting

4.2.3.2. System Integration

4.2.3.3. Operation and Management

4.3. North America Cloud Access Security Brokers Market Analysis, By Cloud Deployment Type, 2014 – 2024 (US$ Bn)

4.3.1. Overview

4.3.2. Software as a Service (SaaS)

4.3.3. Platform as a Service (PaaS)

4.3.4. Infrastructure as a Service (IaaS)

4.4. North America Cloud Access Security Brokers Market Analysis, By Country, 2014 – 2024 (US$ Bn)

4.4.1. Overview

4.4.2. U.S.

4.4.3. Rest of North America

5. Europe Cloud Access Security Brokers Market Analysis, 2014 – 2024 (US$ Bn)

5.1. Overview

5.2. Europe Cloud Access Security Brokers Market Analysis, By Components, 2014 – 2024 (US$ Bn)

5.2.1. Overview

5.2.2. Software

5.2.2.1. On-premise

5.2.2.1.1. Control and Monitoring

5.2.2.1.2. Risk and Compliance Management

5.2.2.1.3. Cloud Data Encryption

5.2.2.1.4. Data Leakage Prevention

5.2.2.1.5. Tokenization

5.2.2.2. Cloud

5.2.2.2.1. Control and Monitoring

5.2.2.2.2. Risk and Compliance Management

5.2.2.2.3. Cloud Data Encryption

5.2.2.2.4. Data Leakage Prevention

5.2.2.2.5. Tokenization

5.2.3. Services

5.2.3.1. Consulting

5.2.3.2. System Integration

5.2.3.3. Operation and Management

5.3. Europe Cloud Access Security Brokers Market Analysis, By Cloud Deployment Type, 2014 – 2024 (US$ Bn)

5.3.1. Overview

5.3.2. Software as a Service (SaaS)

5.3.3. Platform as a Service (PaaS)

5.3.4. Infrastructure as a Service (IaaS)

5.4. Europe Cloud Access Security Brokers Market Analysis, By Country, 2014 – 2024 (US$ Bn)

5.4.1. Overview

5.4.2. EU7 (The UK, Italy, Spain, France, Germany, Belgium, and the Netherlands)

5.4.3. CIS

5.4.4. Rest of Europe

6. Asia Pacific Cloud Access Security Brokers Market Analysis, 2014 – 2024 (US$ Bn)

6.1. Overview

6.2. Asia Pacific Cloud Access Security Brokers Market Analysis, By Components, 2014 – 2024 (US$ Bn)

6.2.1. Overview

6.2.2. Software

6.2.2.1. On-premise

6.2.2.1.1. Control and Monitoring

6.2.2.1.2. Risk and Compliance Management

6.2.2.1.3. Cloud Data Encryption

6.2.2.1.4. Data Leakage Prevention

6.2.2.1.5. Tokenization

6.2.2.2. Cloud

6.2.2.2.1. Control and Monitoring

6.2.2.2.2. Risk and Compliance Management

6.2.2.2.3. Cloud Data Encryption

6.2.2.2.4. Data Leakage Prevention

6.2.2.2.5. Tokenization

6.2.3. Services

6.2.3.1. Consulting

6.2.3.2. System Integration

6.2.3.3. Operation and Management

6.3. Asia Pacific Cloud Access Security Brokers Market Analysis, By Cloud Deployment Type, 2014 – 2024 (US$ Bn)

6.3.1. Overview

6.3.2. Software as a Service (SaaS)

6.3.3. Platform as a Service (PaaS)

6.3.4. Infrastructure as a Service (IaaS)

6.4. Asia Pacific Cloud Access Security Brokers Market Analysis, By Country, 2014 – 2024 (US$ Bn)

6.4.1. Overview

6.4.2. Japan

6.4.3. China

6.4.4. South East Asia

6.4.5. Rest of APAC

7. Middle-East & Africa (MEA) Cloud Access Security Brokers Market Analysis, 2014 – 2024 (US$ Bn)

7.1. Overview

7.2. MEA Cloud Access Security Brokers Market Analysis, By Components, 2014 – 2024 (US$ Bn)

7.2.1. Overview

7.2.2. Software

7.2.2.1. On-premise

7.2.2.1.1. Control and Monitoring

7.2.2.1.2. Risk and Compliance Management

7.2.2.1.3. Cloud Data Encryption

7.2.2.1.4. Data Leakage Prevention

7.2.2.1.5. Tokenization

7.2.2.2. Cloud

7.2.2.2.1. Control and Monitoring

7.2.2.2.2. Risk and Compliance Management

7.2.2.2.3. Cloud Data Encryption

7.2.2.2.4. Data Leakage Prevention

7.2.2.2.5. Tokenization

7.2.3. Services

7.2.3.1. Consulting

7.2.3.2. System Integration

7.2.3.3. Operation and Management

7.3. MEA Cloud Access Security Brokers Market Analysis, By Cloud Deployment Type, 2014 – 2024 (US$ Bn)

7.3.1. Overview

7.3.2. Software as a Service (SaaS)

7.3.3. Platform as a Service (PaaS)

7.3.4. Infrastructure as a Service (IaaS)

7.4. MEA Cloud Access Security Brokers Market Analysis, By Country, 2014 – 2024 (US$ Bn)

7.4.1. Overview

7.4.2. GCC Countries

7.4.3. Southern Africa

7.4.4. Rest of MEA

8. Latin America Cloud Access Security Brokers Market Analysis, 2014 – 2024 (US$ Bn)

8.1. Overview

8.2. Latin America Cloud Access Security Brokers Market Analysis, By Components, 2014 – 2024 (US$ Bn)

8.2.1. Overview

8.2.2. Software

8.2.2.1. On-premise

8.2.2.1.1. Control and Monitoring

8.2.2.1.2. Risk and Compliance Management

8.2.2.1.3. Cloud Data Encryption

8.2.2.1.4. Data Leakage Prevention

8.2.2.1.5. Tokenization

8.2.2.2. Cloud

8.2.2.2.1. Control and Monitoring

8.2.2.2.2. Risk and Compliance Management

8.2.2.2.3. Cloud Data Encryption

8.2.2.2.4. Data Leakage Prevention

8.2.2.2.5. Tokenization

8.2.3. Services

8.2.3.1. Consulting

8.2.3.2. System Integration

8.2.3.3. Operation and Management

8.3. Latin America Cloud Access Security Brokers Market Analysis, By Cloud Deployment Type, 2014 – 2024 (US$ Bn)

8.3.1. Overview

8.3.2. Software as a Service (SaaS)

8.3.3. Platform as a Service (PaaS)

8.3.4. Infrastructure as a Service (IaaS)

8.4. Latin America Cloud Access Security Brokers Market Analysis, By Country, 2014 – 2024 (US$ Bn)

8.4.1. Overview

8.4.2. Brazil

8.4.3. Rest of Latin America

9. Company Profiles

9.1. NetSkope Inc.

9.1.1. Company Details (HQ, Foundation Year, Employee Strength)

9.1.2. Market Presence, By Segment and Geography

9.1.3. Key Developments

9.1.4. Strategy and Historical Roadmap

9.1.5. Revenue and Operating Profits

* Similar details would be provided for all the players mentioned below

9.2. Skyhigh Networks

9.3. CloudLock Inc.

9.4. Zscaler, Inc.

9.5. Adallom, Inc.

9.6. Bitglass, Inc.

9.7. CipherCloud Inc.

9.8. Protegrity USA, Inc.

Copyright © Transparency Market Research, Inc. All Rights reserved

Trust Online

Cloud Access Security Brokers Market